The Cost of Chasing Investment Performance

“Comparison is the thief of joy.”

-Theodore Roosevelt, 26th President of the United States

I don’t know the context of Mr. Roosevelt’s comment, but this quote has been one of my favorites because of its elegance in addressing some things that affect all of us. In my life and career, I have thought a lot about how comparison can be a double-edged sword. On one hand, it’s a healthy measure for helping us reach personal goals and staying aligned to our personal values. On the other, it can drive us to worry about things we cannot control. When it comes to our finances, it can be detrimental to our long-term goals.

In high school, I had a friend, whom I’ll call Tom. Tom was accomplished. He played the violin, was a good athlete and was excellent academically. Although Tom did his best in every subject and his report card was good term after term, it was never good enough for his parents. Tom would come home with an A+ (95%+) in math and sciences but his parents would say, “what happened to the other 5%?”, or “you know your cousin got 100% in biology?” Luckily, Tom turned out “normal”. He’s a successful engineer and has a nice family. Fortunately, Tom kept a positive perspective on his parent’s comments. He knew it was just their way of encouraging him to do better. Had Tom a different perspective, I’m sure these unrealistic expectations could have crushed him or caused him to take a different path in life.

Investors suffer from the same affliction as Tom’s parents and it often leads to poor decisions, lower returns and a less comfortable retirement.

A real-life investment example comes to mind. From 1997 to the first quarter of 2000, value managers had a tough go. Old economy stocks were passé and anything internet related was on fire. Clients were firing their value managers to go to growth managers. One particular client – let’s call him Bob (I’m sure there were many) had the unfortunate timing of doing so in March 2000, at the height of the Technology bubble. This cost them dearly. How much? Let’s look at the below chart:

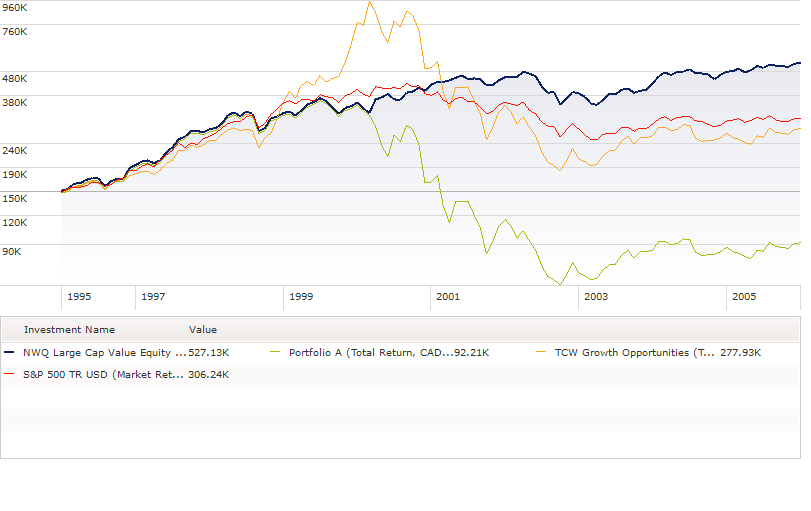

Untimely Switching: The Impact on Performance

Bob’s Returns: January 1996 to December 2005

Bob invested in a value-style fund on January 1, 1996 and held it through February 28, 2000, when he switched to a growth-style fund on March 1, 2000 and held that through December 31, 2005. The chart shows Bob’s dilemma. From the end of 1998 through to the end of 1999, the value fund lagged the growth fund considerably. The temptation to chase returns was obviously very strong and Bob’s switch cost him considerably. At the end of the 10-year period, he had lost nearly 40% of his initial investment. Had he not made the switch, his portfolio would have grown by 251%, handsomely beating the growth of the S&P 500 of 104% and even the results of the growth fund’s 85%. Now, you may be a disciplined investor and would never chase returns, but let’s look at how the average investor tends to behave.

According to Dalbar, a Massachusetts research firm that has studied the behavior of mutual fund investors for the past 26 years, the average investor underperformed the markets for both stocks and bonds over the past year, five, 10, 20 and 30 years.

Comparatively, through December 31, 2018, the average investor underperformed by:

- 5.88 percentage points, annualized, over 30 years (455% less total wealth);

- 3.46 percentage points, annualized, over 10 years (41% less total wealth);

- 4.35 percentage points, annualized over five years. (24% less total wealth)

(Source: 2018 Dalbar Quantitative Analysis of Investor Behavior)

Dalbar outlines several negative behaviours that cause this, but two of the biggest were:

• Leaving the market during volatile periods; and

• Performance chasing (i.e. switching current investments for ones that had done better recently).

Dalbar’s data leads to the inescapable conclusion that most investors suffer from performance anxiety. We make incorrect conclusions about performance and we panic, making ourselves poorer in the process. Thankfully though, there is help.

Another study, for example, finds that investors working with a (non-robo) financial advisor boosted their investment returns by 3% per year.

About half of this benefit came from “behavioral coaching,” which the study identified as the most influential action an advisor can take.

The Right Price for Value or Growth

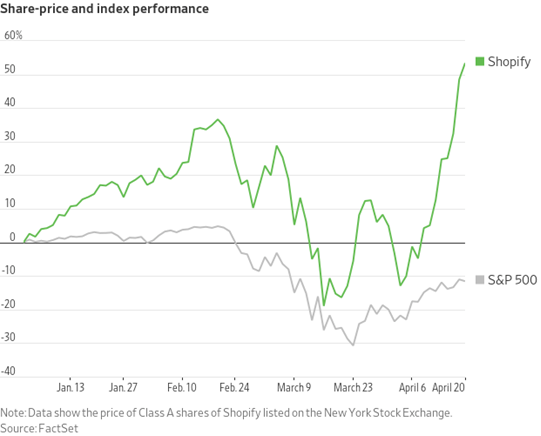

I discussed the dynamics of the oil markets in my last letter. I believe those dynamics will be with us for quite some time, at least until the supply and demand imbalances adjust. However, another interesting dynamic has been occurring. The market is punishing value and high dividend yield stocks more than expensive growth stocks. That is disappointing news for value managers who have been waiting a long time to say "I told you so" to momentum and growth investors. Take the following example of Canadian company Shopify.

Share Price and Index Performance

Shares of Shopify hit a record last week, cresting at US$630 as investors scrambled for any winners in the stay-at-home economy that has resulted from the pandemic.

Shopify, which publishes and sells software for online commerce, has a business tailor-made for a time when social distancing requires consumers to do most of their buying online. Sales have been up every year since it went public in 2015. It has about $2.5 billion in cash on the books and almost no long-term debt. On the other hand, Shopify earned “only” $770,000 in the fourth quarter of 2019, and that was its first profitable quarter since going public.

In a past weekly letter, I covered the concept of price vs. value, so let’s explore that further. As a business, Shopify has tremendous potential. What investors should think about is how much they are paying for that potential. Today, for every dollar of projected earnings (consensus forecasts by equity analysts), an investor is paying $3,333.33. We call this the price-to-earnings (P/E) ratio and it gives us one way to compare the relative expensiveness or cheapness of companies. Growth stocks are typically more expensive than the overall stock market, but a PE ratio of 3,333x is extraordinary.

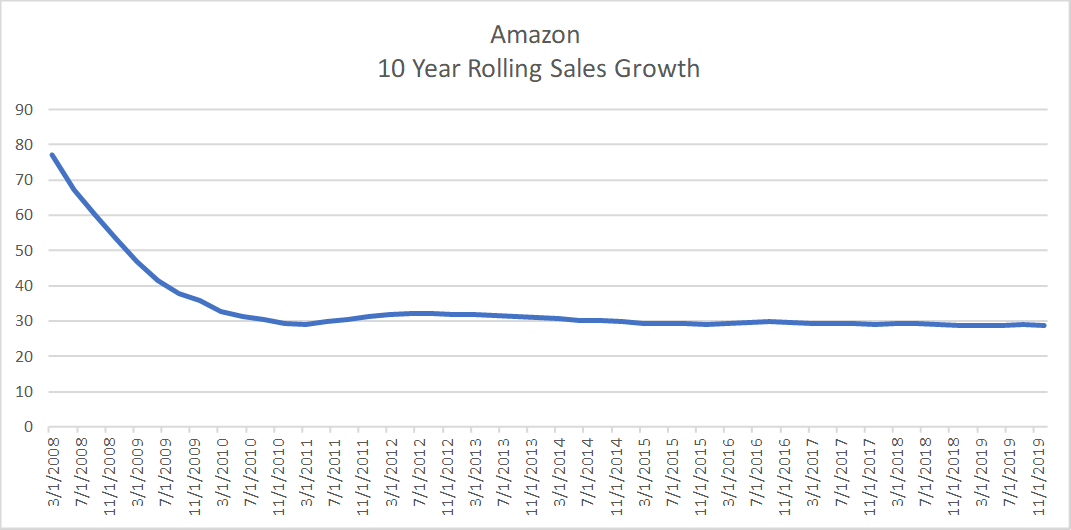

A growing company is typically reinvesting into its business and doesn’t have any earnings, so looking at a metric like price-to-sales (P/S) ratio and comparing it to another successful company like Amazon would be more appropriate. Amazon has grown to be the largest company in the world, but it has not produced much value in the way of profits or earnings over the past 20 years as it has reinvested back into the business. But most investors would agree that Amazon has created phenomenal value along the way.

Currently, Shopify has a P/S of 46x, while Amazon has a P/S ratio of 4.33x. This implies that investors are assuming that Shopify will continue to grow unabated at a rate of 101% per year over the next 10 years in order for that P/S ratio to be equal to Amazon. Is a growth rate of 101% each year over the next 10 years reasonable? I don’t know for certain, but looking at Amazon’s historical growth rate over 10-year rolling periods, I would say that it may be a stretch.

Source: Bloomberg

I’m not saying that Shopify or other growth stocks shouldn’t be in an investor’s portfolio - we certainly do have them in ours - but in measured quantities and with a full understanding of the risk/return trade-offs. Today, investors are crowding into companies that they believe to be structural winners due to the impact of social distancing, but do their growth assumptions make sense? This brings back memories of the Tech bubble in 1999-2000 when analysts found new metrics, such as “price-to-eyeballs,” to justify the market cap of businesses such as Pets.com.

During every crisis, investors abandon adherence to fundamentals on the premise that they are in unique times and instead chase price.

True, it is difficult to measure what will be the full impact on a company throughout a crisis. However, investors ultimately have to make judgements about whether the company will come out of the crisis and, if it does, what it will generate in earnings to make sensible investment decisions.

Is Inflation Lurking Around the Corner?

Some observers argue that once the pandemic passes, record fiscal deficits, debt sustainability concerns and higher inflation will push interest rates back up to, and potentially even above, pre-pandemic levels. Others believe that a combination of a larger private sector savings glut and something economists call yield curve control by central banks will keep interest rates low long after the pandemic has passed. So, which is it? In my April 15 letter, I provided our view on inflation, but I think this topic is so important that we should look at it a little more.

It’s far too soon to worry about inflation given the immediate humanitarian need for disaster relief. Many millions of newly unemployed people need cash now just to pay bills and buy food for themselves and their families.

Hesitating to provide help now because of inflation later would be morally wrong and is likely to set up our society for further disaster.

Approximately 26 million people across the US filed for unemployment insurance during the five-week period ending April 23. In Canada, that number was 7.8 million at last count and climbing quickly.

When people lose their jobs, they immediately cut back on discretionary spending while those who have jobs tend to reduce spending as a precaution. My family has cut back our spending. Vacations are cancelled. Restaurant meals are zero for the month and my gasoline consumption is less than one tank’s worth. Have you increased or decreased your spending over recent weeks? This sudden decline in spending reduces demand much lower than supply and thereby puts downward pressure on the prices of goods and services. Unsurprisingly, inflation expectations have dropped. According to the Bank of Canada in its April 15 update, inflation is expected to be close to zero per cent in the second quarter of 2020.

Fiscal stimulus is necessary to keep our economy functioning through this health crisis. By putting money in people’s hands, governments are propping up demand and preventing a larger than necessary decline in economic output. Failing to do so would risk a depression and profound human suffering.

It is true that when tax receipts tumble and government spending soars, deficits and debt expand.

How much new debt will be created? Economists say Canada’s federal government is headed for a $180-billion deficit this year― about seven times larger than the previous year’s deficit. But rock-bottom interest rates likely mean this massive new IOU will “only” cost taxpayers around $1 billion a year to service.

You might be saying that printing money is inflationary, and you would be right – if the value of output and consumption were otherwise the same. But in this crisis, not only is consumption declining, but we are also losing productivity every day. If today’s money printing succeeds in maintaining the current value of consumption spending, then there would be many more dollars chasing fewer goods and services, and the result would be inflation. However, consumption has declined in line with the value of lost output.

In our view, we shouldn’t be worried about the quantitative easing policies by the Bank of Canada or the U.S. Federal Reserve.

It won’t be inflationary. We should be aware of and concerned about fiscal policy conducted by our governments. If they are imprudent about deficit spending beyond this crisis, then we should be concerned. After the economy recovers to full employment, ongoing high levels of deficit spending would be inflationary. Will our governments have the foresight and will to be prudent? I hope so. Whatever comes, as I have mentioned in my previous notes, we will manage through it.

Final Thoughts

I know that the last several weeks have been difficult for everyone, not just on a personal level but also on the economic front. As social beings, we are growing tired of being apart and we long for going back to the way things were. We see the evidence of that in the U.S., where there are protests over social distancing. Closer to home, with the warm weather this past Saturday in southern Ontario, I saw a dramatic increase in the number of people out and about.

Personally, every day feels like ground hog day. The routine is the same. Video conference calls weigh on me. I think I’m getting ‘Zoom Fatigue’. As you have heard me say, I long for the outdoors. I’m sure many of you feel the same way. My fear is that we may abandon our discipline and, as a result, it may cost us in the long term. Japan’s northern island of Hokkaido offers a grim lesson of what happens when restrictions are lifted too swiftly. Hokkaido acted quickly and contained an early outbreak of the coronavirus with a three-week lockdown. But, when the governor lifted restrictions, a second wave of infections hit even harder and, 26 days later, the island was forced back into lockdown. Let’s stay disciplined. Just like investing, this is going to be hard. There are no easy shortcuts to battling COVID-19 or to achieving your long-term goals.

Whatever your investments, when you are feeling that itch to chase performance, or make performance comparisons, remember that comparisons can be a double-edged sword if you don’t understand what drove that performance and why. Equally, it’s important to go back to the fundamental reasons of how your investments fit into your financial plan and assess whether they are keeping you on track to meeting your goals.

Until next week, stay safe and be well.

Corrado Tiralongo

Chief Investment Officer

Counsel Portfolio Services | IPC Private Wealth

Click Here to Read Our Forward-Looking Statements Disclaimer